The 2025 Investment Outlook for Financial Advisors

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZWMLDPGTLNGK5L72GEJY6R3UHI.png "The 2025 Investment Outlook for Financial Advisors")

What will look different about the investing landscape in 2025? With inflation diminishing and interest rates starting to come down, attractive opportunities, as well as risky ones, will present themselves to investors.

What probably won’t look different is massive spending on artificial intelligence by technology companies and the volatility of asset prices. Regardless of what changes, what remains timeless is the importance of creating portfolios that meet your clients’ long-term investment goals as opposed to chasing headlines and returns.

To help you succeed in the year ahead, this outlook brings together the research and insights of analysts across Morningstar. For 2025, we will focus on areas that address a key challenge or opportunity.

- Our best investing ideas when the US looks expensive.

- Finding returns in a falling rate environment.

- The pros and cons of investing in private assets.

- The impact of AI on investing in 2025.

The following information was adapted from the work of Morningstar research teams and their robust 2025 outlook report.

Our Best Investing Ideas When the US Looks Expensive

In 2024, US stocks once again outpaced the rest of the world, rising over 25%, fueled by the strong performance of stocks that benefit from the AI boom and the prospect of lower interest rates. However, valuations for US stocks now appear expensive based on both Morningstar stock-level valuation models and top-down expected return estimates.

As we look for opportunities heading into 2025, our focus naturally shifts to regions outside the United States, where we believe investors may achieve better risk-adjusted returns. Our asset-class valuation models point to low-single-digit returns in the United States, while we expect some of the most attractive opportunities abroad to deliver double-digit returns over the next decade.

The medium-term prospects for Chinese equities are reason for optimism. Despite a bleak situation over recent years and a bumpy road still ahead, we’re encouraged by signs the authorities are prioritizing policy support to shore up the economy. The situation only needs to become a little better there to see returns.

We view Europe, and the United Kingdom in particular, as the most attractive developed-markets region globally. Small-cap stocks, for instance, offer much greater value than their large-cap peers, trading at a whopping 40% discount to their fair value estimate. On a sector basis, the standout area is consumer.

Even when accounting for elevated uncertainty in Mexico, we believe that market provides a decent entry point for long-term investors as valuations look attractive, particularly given much of the future cash flows are coming from stable, defensive sectors.

Brazil is one of the most cyclically oriented markets we follow, and earnings will undoubtedly ebb and flow with the global economy. But for those willing to invest through the cycle, this market’s cheap valuation offers a margin of safety not often found.

Macroeconomic and political concerns often sully emerging markets. But for long-term-oriented investors, a period of uncertainty can often be a great time to buy, particularly for those investors with the ability to ride out short-term volatility.

Morningstar Tips for Advisors

- Screen for funds with more international exposure with investment research tools. What’s on your product shelf, and how does it compare with what’s in client portfolios?

- Review client portfolios for opportunities where clients might be overallocated to domestic stocks.

- Keep an eye on evolving economic policy in China, which could make the country’s stocks more popular.

- Don’t avoid US stocks altogether but consider unloved areas of the US market as well.

- Consider high-quality government-yield bonds, which remain one of the most reliable assets to hold for diversifying equity risk in periods of weak growth or recessions.

Finding Returns in a Falling Rate Environment

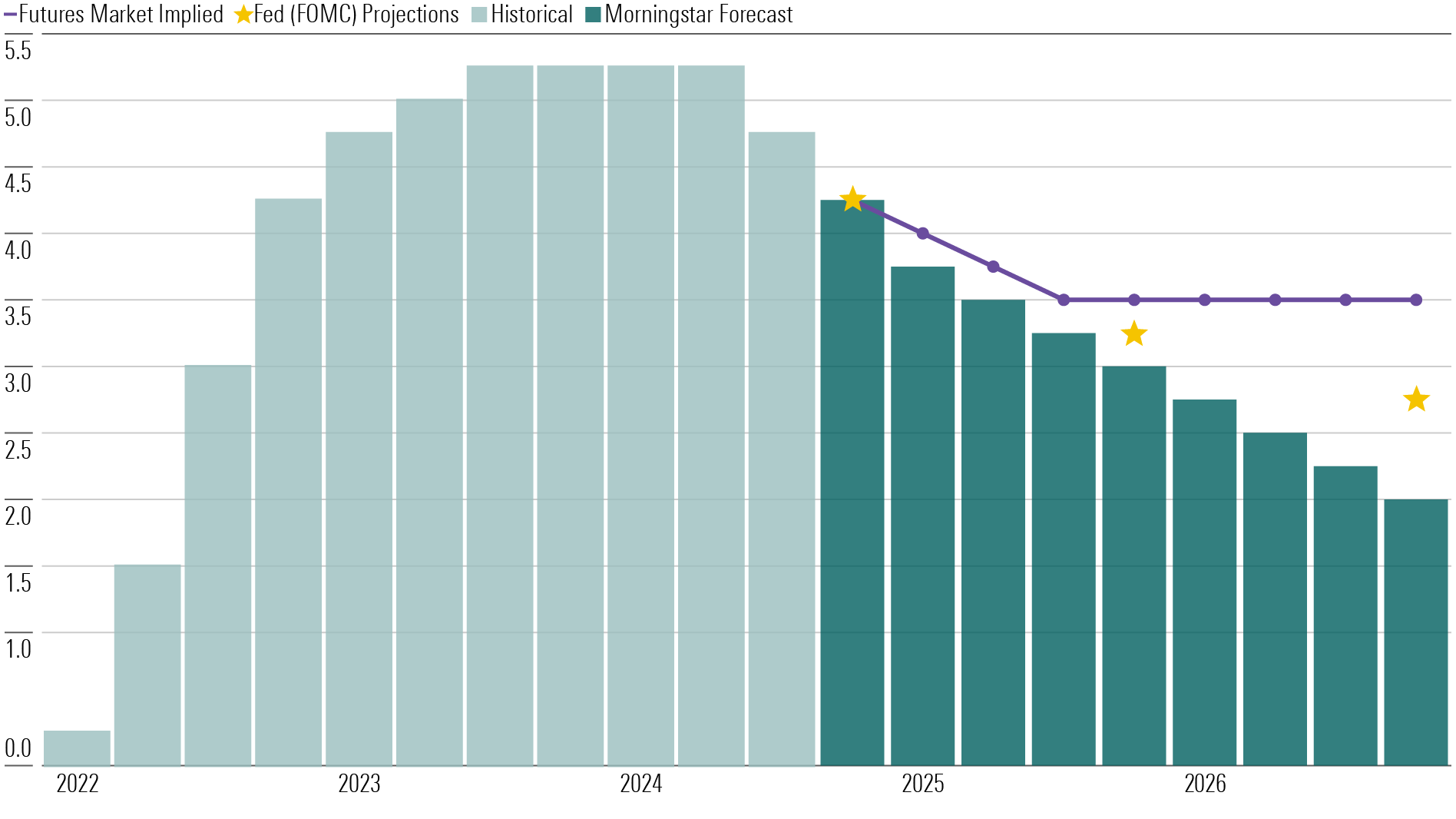

With inflation on the downtrend and cash rates expected to fall around the globe, investors might be uncertain of where to position the fixed-income portion of their portfolios.

Morningstar economists expect the federal-funds rate to fall from the 5.25%-5.50% range to 4.25%-4.50% at the end of 2024, 3.00%-3.25% at the end of 2025, and 2.00%-2.25% at the end of 2026, substantially reducing the income that bank deposits can generate.

For a long-term investor, holding too much cash has historically led to lower long-term portfolio returns compared with nearly all other fixed-income asset classes. Should our federal-funds rate forecast play out, investors would benefit by holding longer-term fixed-income bonds to maintain higher income levels.

Moreover, we expect the federal-funds rate to average 2.3% over the next 10 years. Consequently, longer-term government bonds appear to offer an unusually high return relative to cash deposits.

In contrast to government bonds, corporate debt offers unusually low returns for the additional risk that an owner must accept. We can use credit spreads, which measure the additional yield that investors can expect with additional credit risk, as a proxy for valuations. The tighter the spreads, the more costly credit assets are. Our data points to an asymmetrical risk profile for credit assets: limited upside because of historically tight spreads and significant downside risk should the economy experience a hard landing.

Outside of the US, we see some opportunities to add diversification and attractive yields to portfolios via global sovereign bonds. A simple rule of thumb when investing across the global-bond universe is to focus on real yields. In other words, look where nominal yields are higher than prevailing inflation and central bank inflation targets.

Morningstar Tips for Advisors

- Talk to clients about adding a little duration to their portfolios. Should our federal-funds rate forecast play out, investors would benefit by holding longer-term fixed-income bonds to maintain higher income levels.

- Set client expectations on how fixed-income funds will perform in a lower interest-rate environment. Corporate debt in particular offers unusually low returns for the additional risk an owner must accept. Financial Industry Regulatory Authority-compliant reports on hypothetical performance can show how portfolios may perform in a range of environments.

- Sprinkle in some emerging-markets debt. Outside of the United States, we see some opportunities to add diversification and attractive yields to portfolios via global sovereign bonds.

- We believe looking to assets outside of fixed income as diversifiers may be wise given the uncertainty regarding inflation and interest rates, which has been amplified given the 2024 US presidential election results.

- Don’t overthink short-term economic and political events like elections. The sentiments stemming from them tend to remain short-lived.

The Pros and Cons of Investing in Private Assets

While we applaud efforts to meet investor demand, two areas of public and private market convergence will draw our focus in 2025 and beyond:

- The liquidity risks associated with bringing private assets to retail products.

- The potential costs associated with this convergence.

Most of the industry buzz right now is around investment products that directly own private-company shares. These products face significant structural challenges, though. So far, the handful of interval funds in the United States that directly own private-company equity shares have not produced impressive returns.

When it comes to retail investor exposure to private assets, retirement or pension funds offer some insight. Australia’s superannuation pension system funds have been pioneers in classes such as unlisted infrastructure and property, having successfully allocated to these classes for decades. Private credit has rapidly gained traction, suggesting its relatively small allocation is likely to increase over time.

By allocating to private assets, Australian pension funds are playing to their strengths; their long-term investment horizons and liquidity profiles neatly align with those of private assets. Liquidity, one of the key drawbacks of private assets, is less of an obstacle for pension funds, and the benefits of the asset class can be more freely utilized.

Morningstar Tips for Advisors

- Keep an eye on fees associated with convergent funds. Competition among asset managers to lead this public and private convergence should drive fees lower and create better products.

- Be mindful of the liquidity risks and constraints that are associated with bringing private assets to retail products.

- Prepare for client conversations about private-market investments. Investors might be more likely to ask about opportunities as industry chatter mounts. Background research will establish you as an expert on emerging trends.

The Impact of AI on Investing in 2025

Suppliers of graphics processing units and hardware like Nvidia NVDA have invested tens of billions of dollars to build out their capacity. Knowing that, we expect 2025 could be the year capacity begins to catch up to demand and the next evolution of AI will begin.

The next step will be for corporations to embed AI within their products and for services to drive revenue growth. Those companies that drive revenue and/or expand operating margins will not only provide earnings growth today but will help those companies to either dig or widen their economic moats to bolster returns on invested capital for years to come.

Artificial Intelligence: Financial Advisor Use Case

On a different note, we thought it would be instructive to provide a use case of how financial advisors are beginning to use AI within their practice. If advisors are after more face time with clients, they can get back crucial hours by using AI to reduce the load of administrative tasks, client meeting preparation, compliance, and investment research.

Some advisors use generative AI to take notes during client meetings and summarize the meeting afterward, saving time both following a meeting and preparing for the next one. Other advisors may use generative AI to help create a first draft of educational materials they distribute to clients.

However, Morningstar research has found that certain use cases of generative AI, like personalizing emails or financial recommendations, can have a negative impact on the advisor-client relationship. Whether using AI for your own benefit or investing in those companies that will be able to leverage the power of AI, understanding the evolution of the scope and use cases for AI will be instrumental in 2025.

Morningstar Tips for Advisors

- Take a look at the companies being supplied by Nvidia, Amazon.com AMZN, Alphabet GOOGL GOOG, and Microsoft MSFT as potential sources of AI-influenced returns.

- Consider using AI for administrative tasks to free up time for in-person client meetings. In Advisor Workstation, the digital assistant Mo can help screen for investments and navigate the platform faster than ever.

- Be cautious of overdoing it with AI. It may not be appropriate for personalized financial recommendations.

Food for Thought as We Enter 2025

As we enter 2025, our analysts are wary of some US stocks but optimistic about equity opportunities abroad. They also think high-quality government bonds could be a useful tool in diversifying a portfolio and staying ahead of inflation. Finally, they encourage investors not to overreact to short-term geopolitical conditions, such as elections.

The comprehensive 2025 outlook delves into all of these key issues and more in much greater depth.

Research Contributors

The report and this article include contributions from: Philip Straehl, James Foot, Lochlan Halloway, Michael Field, Nick Stanhope, Dominic Pappalardo, Preston Caldwell, Hong Cheng, Mark Preskett, Brian Moriarty, Jack Shannon, Thomas Dutka, David Sekera, Timothy Strauts, Danielle Labotka, Eric Compton, Brian Colello, Dan Romanoff, Ricky Williamson, Sean Neethling, Michael Malseed, Samantha Lamas, Mike Coop, Matt Wacher, Michael Budzinski, and Nicoló Bragazza.

link